The Government of Bahrain has announced a series of initiatives aimed at improving the country’s financial situation while ensuring continued support for citizens. The measures, approved by the Cabinet, focus on optimizing government spending, increasing revenue, and promoting sustainable economic growth. The initiatives include:

Corporate Revenue Law

Reducing Administrative Expenses

All government entities will cut administrative costs by 20% while maintaining the service quality of services provided to citizens.

Increasing Contributions from State-Owned Companies

Government-owned companies will contribute more to the state budget.

Selective Tax on Soft Drinks

A law will be referred to the legislature to increase selective taxes on soft drinks, promoting healthier consumption, improving public health, and optimizing healthcare resources.

Investment Land Fees

Sewerage Service Fees

Work Permit Fees for Foreigners

Search

Recent Insights

UAE VAT Update: Introduction of Reverse charge mechanism on Metal Scrap Trading among registrants in the state for the purpose of VAT (Effective From 14th January 2026)

The Federal Tax Authority (FTA) has introduced an important update on the VAT treatment of metal scrap supplies through Cabinet Decision No. 153 of 2025, issued on November 14, 2025, and effective from January 14, 2026. The decision mandates the application of the Reverse Charge Mechanism (RCM) on metal scrap transactions between VAT-registered persons.

Under the decision, the reverse-charge mechanism will apply to eligible supplies between registrants within the metal-scrap sector.

Prior to this decision, supplies of metal scrap were treated as normal taxable supplies for UAE VAT purposes and were subject to either the standard rate or zero rate, depending on the nature of the supply, such as whether it was a local supply or an export.

Particulars Type | Old rule (Before 14 Jan 2026) | New rule (After 14 Jan 2026) |

|---|---|---|

VAT charged on Invoice | Standard Rated (5%)/ Zero rated (0%) | No VAT Charged |

Invoice Type | Tax Invoice | Tax Invoice (RCM Reference) |

Responsibility of VAT Reporting | Supplier | Buyer (Under RCM) |

Declaration | Not Required | Mandatory |

Compliance Risk | Normal | Higher (Due to documentation Requirement) |

Buyer (Prior to supply)

Supplier (Prior to supply)

Failure to meet these requirements will result in the application of normal VAT rules.

*Declaration Format not issued by FTA specifically for the Metal Scrap sector till now.

Cash Flow: Buyers will no longer need to pay VAT on purchases, and suppliers will not be required to charge output VAT on supplies.

Compliance Responsibility: Both suppliers and buyers are required to maintain and obtain proper documentation

Changes in Business Process: Business must update the invoicing system, internal controls and contracts before January 2026.

Recommended Action Plan

The Introduction of the reverse charge mechanism on metal scrap trading mark a significant shift in the UAE VAT framework. These changes transfer the VAT accounting responsibility from the supplier to VAT-registered buyers, while placing greater emphasis on documentation and verification procedures.

Businesses involved in metal scrap transactions must take proper steps to assess the impact of this change, update their system and contacts and ensure that all required declarations and controls are in place.

Search

Recent Insights

The Ministry of Finance issued two key legislative updates in October 2025:

Effective date of the amendments: January 01, 2026

Article 48(1) – Reverse Charge

Overview of the Amendment:

Taxable Person imports Goods or Services for the purposes of his Business, then he shall be treated as making a Taxable Supply to himself. It is therefore responsible for calculating and paying the VAT liable on this supply. The Key change is that the company does not have to send itself a tax invoice for these imported goods or services.

It is important to note that despite the amendment, self-invoicing may still be required in certain cases to facilitate recovery (where supplier invoice/documents may not be available).

Implications:

Article 54 – Recoverable Input Tax (New anti-tax-evasion provisions introduced)

Overview of the Amendment:

Implications:

Article 74(3) – Excess Recoverable Tax.

Overview of the Amendment:

Implications:

Transitional Provision allowing one year window until December 31, 2026

Overview of the Amendment:

Taxpayers whose five-year claim period has expired or will expire within one year of the Decree-Law’s effective date can still request a refund or apply credit balances toward tax due or penalties.

With the introduction of the amendments (including transitional relief), businesses have a limited window until 31 December 2026 to claim refunds for tax periods 2018–2020. After this date, the right to recover these amounts will permanently expire.

Business Implications:

Businesses should promptly review VAT records for FY 2018–2020, as any unclaimed input tax must be recovered by 31 December 2026. Amounts not claimed by this deadline will be permanently lost, adversely impacting cash flow.

Illustrations 1

Scenario

Application of the Amendment

Illustrations 2

Scenario

Application of the Amendment

Article 79 (bis)

This law has been officially repealed and is no longer applicable.

Article 9 (3) -Determination of Payable tax

Overview of the Amendment:

Taxable Person pays an amount in excess of the Payable Tax, or has a credit balance with the Authority, the Authority may apply such excess or credit balance to settle any outstanding tax or liabilities due to it, within a period not exceeding five (5) years from the end of the relevant Tax Period.

Business Implications:

Article 10(5) -Voluntary Disclosure

Overview of the Amendment:

If a Taxpayer discovers an error or omission in a Tax Return submitted to the authority that does not result in any difference in the amount of Due Tax, such errors are required to be corrected through a Voluntary Disclosure only in the cases specified by the Authority. In all other cases, the Taxpayer may rectify the error in the subsequent VAT return.

Business Implications:

Article 38(1-2)- Application for refund of credit balance

Overview of the Amendment:

Refund claims (which are in excess of due tax and penalties) must be submitted within five years of the relevant tax period.

Article 38(3-6)- Application for refund of credit balance- New Clauses added

Introduces special timelines as an exception to the five-year rule:

Article 46- Statute of limitations

Overview of the Amendment:

Except in certain specific situations, the UAE VAT Law prohibits the tax authorities from auditing a business or issuing a tax assessment for a VAT period after five years have elapsed. If the taxable person submit VAT refund application in the 5th year or on any late VAT credit periods, the FTA can still conduct audit which must be completed within 2 years from when the claim was submitted. Further, voluntary disclosures are generally not allowed to be submitted beyond five years, except in cases where they relate to an unresolved refund application.

Article 54(bis)

Overview of the Amendment:

The FTA may issue official, legally binding directions to clarify VAT interpretation and ensure uniform application across taxpayers.

Practical Measures

Search

Recent Insights

The shipping and logistics sector is the backbone of global trade. In the United Arab Emirates (UAE), this sector holds strategic importance because of the country’s geographical location and its ambition to be a world-class logistics hub connecting Asia, Europe, and Africa. The UAE’s state-of-the-art ports, airports, and free zones have made it a preferred destination for global supply chains and multinational businesses.

With the introduction of Value Added Tax (VAT) in January 2018, companies operating in shipping, freight forwarding, and logistics have had to understand and comply with a new set of tax rules. While the VAT framework is designed to be business-friendly, the sector’s complex mix of local and cross-border services makes it critical for companies to know when to charge VAT, when zero-rating applies, and when a transaction is outside the scope of UAE VAT altogether.

This article explores the key VAT implications for the shipping and logistics industry in the UAE, providing an in-depth understanding of how different services are treated under the law and highlighting practical scenarios that businesses frequently face.

Understanding Shipping and Logistics

A shipping and logistics company is responsible for moving goods efficiently and securely from one location to another, whether within the UAE or across international borders. The services provided in this sector are diverse and often involve multiple stages of a supply chain. Typical activities include:

Because of this wide scope of operations, VAT treatment varies depending on the nature of the service and whether it relates to domestic transportation, international movements, or import/export activities.

Modes of transportation

Modes of transportation include Sea, Air, Road, transportation and multimodal transportation.

Sea Transport

Air Transport

Road Transport

Multimodal Transport (combining different modes)

Shipping Companies

Shipping companies are businesses that specialize in transporting cargo for a fee, primarily via sea using container ships, but also through other modes like air, rail, and road. They play a vital role in global trade by moving goods, such as raw materials and finished products, between different ports and destinations worldwide, ensuring that products reach consumers and industries efficiently and safely.

VAT Treatments

Transactions Type | VAT Applicability | Examples |

|---|---|---|

International Transportation of goods and passengers | 0% | Freight from Jebel Ali to Europe; passenger flight from Dubai to London. |

International Transportation of goods and passengers includes more than one stops | 0% | Shipment Dubai → Riyadh → Cairo → Europe (entire trip qualifies as international). |

Air passenger transport in the state considered as “International Transport Service” | 0% | Abu Dhabi → Dubai leg of a flight continuing to New York. |

Inbound and outbound transportation of passengers and goods (including intra-GCC) | 0% | Inbound and outbound transportation of passengers and goods (including intra-GCC) |

Transport related services for inbound and outbound transportation | 0% | passengers flying out to Saudi Arabia.

|

Transportation starting and ending outside UAE | Out of Scope | Shipping goods directly from India to Oman without transiting through the UAE |

Transport related services for cross border trade | Out of Scope | Goods are shipped directly from India to Oman without passing through the UAE, while the freight is billed by a UAE company. |

Transactions Type | VAT Applicability | Examples |

|---|---|---|

Local Transportation of goods and services | 5% | Trucking goods from Dubai to Abu Dhabi (not linked to import/export). |

Transport related services for local transportation of goods | 5% | Loading, warehousing, and packaging for a domestic delivery. |

Local transport which is part/for the purpose of inbound and outbound transportation | 0% | Trucking goods from Sharjah to Jebel Ali for onward shipment to Europe |

Local transportation of passengers in non-qualifying means of transport | 5% | Tourist desert safari, limousine service. |

Local transportation of passengers in qualifying means of transport | Exempt | Mono Rail, Dubai Metro, Taxi and Bus |

Supply of means of transport for the transportation of passenger and goods | 0% | Sale of a cargo vessel or aircraft for commercial use |

Freight Forwarding Companies

A freight forwarding company acts as an intermediary to manage the complex process of shipping goods internationally by arranging transportation, handling documentation, and coordinating logistics on behalf of a business. They do not own the transport vehicles, but instead use their network of carriers and partners to find the most efficient and cost-effective way to move cargo via sea, air, rail, or road, ensuring it arrives safely and on time.

Usually undertaking the following:

VAT Treatments

Transactions Type | VAT Applicability | Examples |

|---|---|---|

Local transport which is part/for the purpose of inbound and outbound transportation | 0% | Trucking goods from Sharjah to Jebel Ali for onward shipment to USA |

Freight Brocker service fee | 5% | Service fee charged for arranging freight forward service for an international shipment from Jebel Ali to Europe |

Warehousing service for local sales | 5% | Warehousing fee charged for storing goods in the port |

Local transportation of goods and transport related services for local transportation of goods | 5% | Goods transport from Dubai to Sharjah, and Loading, warehousing, and packaging for a domestic delivery. |

Transport related services for cross border transportation | Out of Scope | Shipping goods directly from India to Oman with no UAE leg, freight charges issued UAE Company |

Goods can be moved by air, sea, rail, or road, and the choice of transport depends on factors such as cargo size and how urgently delivery is required. Because international transport supports the UAE’s trade and tourism growth, the VAT law provides zero-rate (0%) VAT on following types of transport and related services.

Under UAE VAT rules, the following supplies are subject to 0% VAT when used for commercial purposes:

Goods and services directly connected to these means of transport—such as operation, repair, maintenance, or conversion—are also zero-rated, provided the conditions of the VAT law are met.

Warehousing

Warehousing services refer to the storage of goods in a designated facility before they are distributed to their final destination, whether to retailers, other businesses, or end consumers. They are a critical component of the global supply chain and logistics sector.

VAT Treatments

Transactions Type | VAT Applicability | Examples |

|---|---|---|

Warehousing service provided to customer in UAE | 5% | A UAE customer stored or used warehouse facility at a warehouse in the port before clearing the goods. |

Packing, re-packing, labelling etc.. | 5% | Re-packing service provided at warehouse for a UAE company. |

Transaction Scenarios and Their VAT Implications

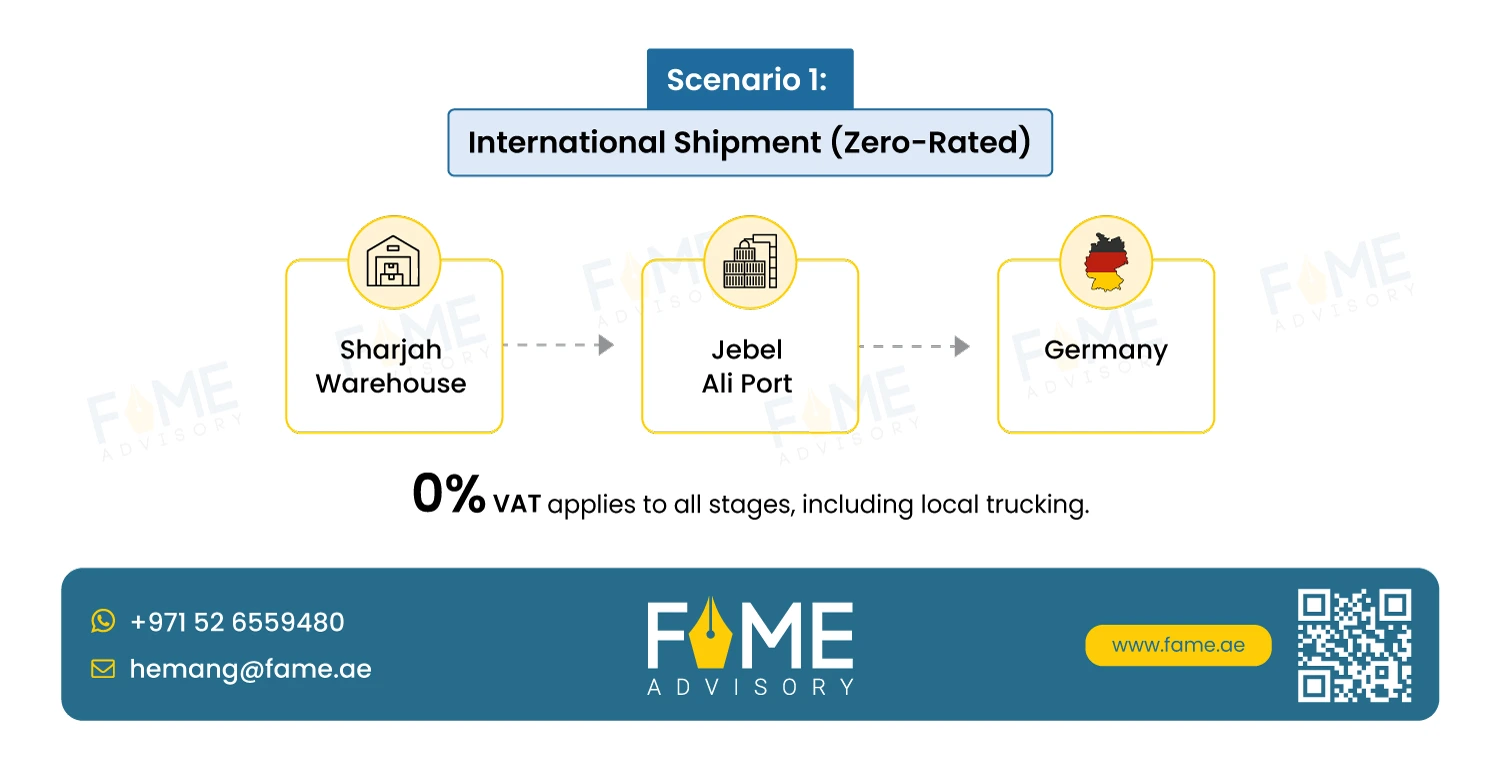

Scenario 1: International Shipment (Zero-Rated)

A freight forwarder arranging shipment of goods from Sharjah to Germany charges 0% VAT, as the service qualifies as international transport.

0% VAT applies to all stages, including local trucking.

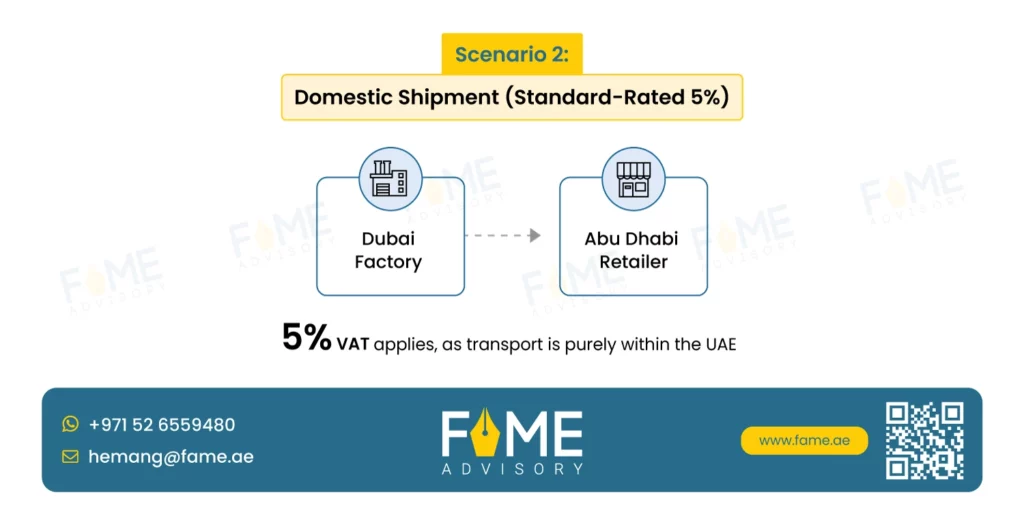

Scenario 2: Domestic Shipment (Standard-Rated 5%)

A trucking company delivering goods from Jebel Ali Free Zone to a retailer in Abu Dhabi applies 5% VAT.

5% VAT applies, as transport is purely within the UAE

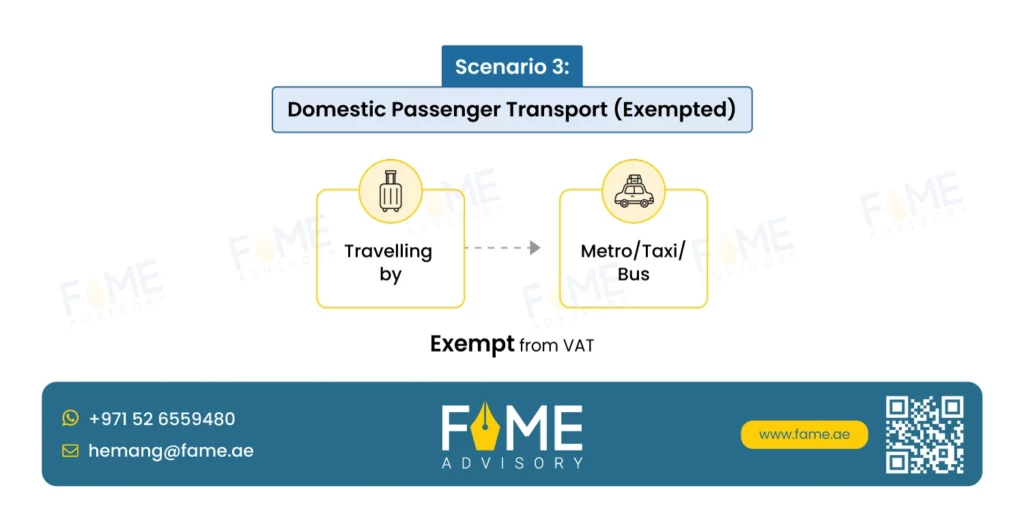

Scenario 3: Domestic Passenger Transport (Exempted)

A metro ride in Dubai is exempt from VAT, but a desert safari tour bus is subject to 5% VAT

Exempt from VAT

Scenario 4: Cross border transport of goods (Out of scope)

A freight forwarder arranging shipment of goods from India to Germany, this will be out of scope of UAE VAT as the transport is not starting or ending in the UAE.

Out of scope of UAE VAT

Conclusion

VAT treatment in the UAE shipping and logistics sector depends on whether the service is domestic, international, exempt, or outside the scope of UAE VAT. To remain compliant and competitive, businesses must apply the correct VAT rate and maintain precise documentation to avoid penalties.

Key compliance priorities for shipping and logistics companies include:

When applied correctly, VAT does not add to the cost of international trade; instead, it promotes transparency, efficiency, and operational integrity. By understanding VAT implications and maintaining robust internal controls, shipping and logistics businesses can remain compliant, cost-effective, and well-positioned to thrive in the UAE’s strategic logistics market.

Search

Recent Insights

On 29th September 2025, the UAE Ministry of Finance took a big step forward in reshaping how businesses handle tax compliance. Two new decisions were issued:

Together, these decisions introduce the Electronic Invoicing System (EIS) – a central, government-run platform designed to move businesses away from manual or paper-based VAT invoicing, and toward structured, digital records that are fast, transparent, and secure.

For businesses, this is not just another compliance requirement. It’s part of a wider transformation toward digitization, transparency, and efficiency in the UAE economy.

What Does E-Invoicing Actually Mean?

Before diving into obligations and deadlines, it’s worth understanding what exactly “electronic invoicing” means in the UAE context. The Ministerial Decisions define several key terms to remove ambiguity and ensure everyone speaks the same language.

1. Electronic Invoice (E-Invoice):

A VAT invoice that is issued, received, transmitted, and stored in a structured digital format. Importantly, this is not just a scanned PDF emailed to a customer. The format is machine-readable, which means it can be validated and processed automatically.

2. Electronic Credit Note:

A digital document that amends or cancels an invoice. This could apply to a return, refund, discount, or correction.

3. Electronic Invoicing System (EIS):

The central platform managed by the Federal Tax Authority (FTA). All e-invoices and e-credit notes must pass through this system for validation, reporting, and storage.

4. Accredited Service Provider:

Businesses will not connect directly to the EIS. Instead, they must use a government-accredited third-party provider who ensures that their ERP or accounting system integrates smoothly with the platform.

5. Excluded Persons and Transactions:

6. Pilot Programme and Taxpayer Working Group:

7. Business-to-Consumer (B2C) Transactions:

8. Revenue:

Why Is the UAE Introducing E-Invoicing?

At first glance, it may seem like this is just another administrative burden. But the reality is quite different. The EIS is being introduced to achieve several strategic objectives:

1. Digitization of VAT Invoicing

2. Improved Compliance

Because the EIS enforces a standard format and real-time reporting, businesses will find it harder to make mistakes or omit information. The FTA will also have more visibility over VAT flows, reducing compliance risks.

3. Transparency and Cooperation

The data collected can be shared with other UAE government departments and even foreign tax authorities under international agreements, boosting trust and credibility.

4. Fraud Prevention

E-invoicing minimizes common issues like false invoicing, duplicate claims, or fraudulent VAT refunds.

5. Alignment with Global Standards

Many countries have already adopted similar systems. By implementing e-invoicing, the UAE is positioning itself within a global ecosystem of modern tax administration, making it easier for multinationals to operate here.

Scope of E-Invoicing:

The decisions make it clear that e-invoicing will apply broadly:

Exemptions

Not every transaction is covered. Key exclusions include:

What Are the Business Obligations?

Once a business is within scope, the obligations under the EIS are detailed and strict:

1. Issuing and Reporting

2. Accredited Service Providers

As per Article 15 of Ministerial Decision No. 64 of 2025 five ARP are approved:

Few more ARP will be added in the above list

3. Data Requirements

4. Special Cases

5. Data Storage

6. System Failures

What Powers Does the FTA Have?

The system will give the Federal Tax Authority significant visibility and control:

This reinforces the dual role of the EIS: enforcing domestic VAT compliance while also supporting the UAE’s global tax transparency commitments.

Phased Implementation Timeline

The transition will not happen overnight. The Ministry has wisely chosen a phased approach:

Phase 1 – Pilot Programme

Phase 2 – Voluntary Adoption

Phase 3 – Mandatory Adoption

Deadlines depend on business size and type:

Enforcement and Penalties

Both decisions came into force immediately after being published in the Official Gazette.

The Bigger Picture

This system is about more than tax reporting. It represents a strategic shift in how the UAE manages taxation and supports its digital economy agenda.

Key benefits include:

Practical Takeaways for Businesses

For companies operating in the UAE, the message is clear: don’t wait until the last minute. Preparing early will not only reduce compliance risks but may also unlock operational efficiencies.

Action to be taken:

Conclusion

Ministerial Decisions No. 243 and 244 of 2025 establish the legal and operational backbone of the UAE’s Electronic Invoicing System. Decision 243 lays out the framework, scope, and obligations, while Decision 244 sets the roadmap for phased adoption.

By 2027, nearly all VAT-registered businesses and government entities in the UAE will be required to issue and process e-invoices through the EIS.

For businesses, this is both a compliance requirement and an opportunity:

Search

Recent Insights

Passenger transportation services are widely used across the UAE, particularly by corporates to facilitate the commute of employees and by hotels to enhance the experience of their guests. While such services appear straightforward, their treatment under the UAE VAT Law requires careful attention.

This article provides a detailed overview of the VAT implications of passenger transportation services in light of Federal Decree-Law No. (8) of 2017 on Value Added Tax (“VAT Law”), Cabinet Decision No. (52) of 2017 on the Executive Regulations (“Executive Regulations”), and its amendments issued by the Federal Tax Authority (FTA).

Legal Basis for Exemption

Article 45 of the Executive Regulations provides that local passenger transport services supplied in a qualifying means of transport (by land, water, or air) are exempt from VAT.

A qualifying means of transport is defined as any Motor vehicle designed or adapted for passenger transportation, including:

Importantly, the legislation does not restrict this exemption only to “public” transportation. Services provided to private groups, such as employees of companies or hotel guests, also qualify for the exemption as long as the core activity is passenger transportation in a qualifying vehicle.

Key Clarifications from the FTA

The FTA has clarified several critical points that businesses should consider when determining the VAT treatment of their transportation services:

Where a business provides transportation services to employees of corporates on a contractual basis using buses or other qualifying means of transport, these services fall within the VAT exemption.

Transport services arranged for hotel guests are also generally exempt. However, businesses must carefully assess the nature of these services. If the principal purpose of the trip is pleasure, leisure, or entertainment (e.g., sightseeing tours or recreational trips), the exemption will not apply, and VAT at the standard rate 5% should be charged.

The exemption strictly applies to the supply of passenger transport services. If a company merely leases or rents buses without providing actual transport services, the arrangement does not qualify for exemption and is subject to VAT at 5%.

Any Value-added services beyond passenger transport are taxable at 5%.

For example:

These ancillary supplies are not covered by the exemption and must be charged at the standard VAT rate at 5%.

Practical Implications for Businesses

Businesses engaged in transportation services must carefully review their contractual arrangements and service structures to determine VAT applicability. Some practical considerations include:

Conclusion

The UAE VAT regime provides an exemption for local passenger transport services when supplied using qualifying means of transport. Importantly, this exemption is not limited to public transport but extends to services for defined groups such as employees of corporates and hotel guests.

However, businesses must draw a clear distinction between exempt passenger transport and taxable supplies such as vehicle leasing or additional services like branding. Incorrect classification could lead to VAT non-compliance and potential penalties.

By carefully reviewing the scope of services, maintaining clear contractual terms, and ensuring accurate VAT treatment, businesses can remain compliant while delivering essential passenger transport solutions across the UAE.

Search

Recent Insights

The Federal Tax Authority (FTA) has issued Ministerial Decision No. 229 of 2025 (MD 229) and Ministerial Decision No. 230 of 2025 (MD 230), introducing significant updates to the definitions of Qualifying Activities and Excluded Activities for Qualifying Free Zone Persons. These decisions repeal and replace Ministerial Decision No. 265 of 2023, particularly updating the Definitions of Qualifying Commodities and other qualifying activities, and provide enhanced clarity for the application of Corporate Tax rules within Free Zones.

Section | Ministerial Decision No. 265 of 2023 | Ministerial Decision No. 229 of 2025 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Changes and Additions to the Definition Section | |||||||||||||

Qualifying Commodities | Earlier in MD 265 the scope was limited to Metals, minerals, energy and agriculture commodities traded on a Recognized Commodities Exchange Market in raw form. | The earlier definition is now broadened and clarifies the scope of the trading of Qualifying Commodities by removing the term “in raw form” and instead allowing the trading of metals, minerals, industrial chemicals, energy and agricultural commodities and Associated By-products, provided that a Quoted Price for such commodities exists.

A Quoted Price is a price of the Qualifying Commodity or a Related Commodity specified by a Recognised Commodity Exchange Market or a Recognised Price Reporting Agency specified by a decision issued by the Minister. (Refer below for the list of Recognised Price Reporting Agencies)

Environmental commodities being tradeable assets that represent a specific environmental benefit (e.g., carbon credits, renewable energy certificates). | |||||||||||

Recognized Commodities Exchange Market | It was described as any commodities exchange market established in the State that is licensed and regulated by the relevant Competent Authority, or any commodities exchange market established and recognized outside the State of equal standing | This has been expanded to also include commodities exchange market established and recognised outside the State that are licensed and regulated by the relevant foreign authority in the jurisdiction of establishment, or as specified in a decision issued by the Minister. | |||||||||||

Competent Authority | MD 265 defined the Competent Authority as only The Central Bank of the United Arab Emirates, the Dubai Financial Services Authority of the Dubai International Financial Centre, the Financial Services Regulatory Authority of the Abu Dhabi Global Market and the Securities and Commodities Authority as applicable. | The definition now has a wider coverage to include all of the earlier authorities plus any other entity as determined by the Minister, as applicable. | |||||||||||

Quoted Price | No such definition was provided earlier | A new definition has now been added as the price of the Qualifying Commodity or a Related Commodity specified by a Recognized Commodity Exchange Market or a recognized price reporting agency** specified by a Ministerial decision. | |||||||||||

Associated By-product | No such definition was provided earlier | Incidental or secondary product made during the production or extraction of the metal, mineral, industrial chemical, energy and agricultural commodity. | |||||||||||

Related Commodity | No such definition was provided earlier | Any commodity that is listed in the same chapter in the Common Schedule for Classification and Coding of Goods as a Qualifying Commodity that has a Quoted Price. | |||||||||||

Common Schedule for Classification and Coding of Goods | No such definition was provided earlier | Classification and Coding of Goods as a Qualifying Commodity that has a Quoted Price.

Common Schedule for Classification and Coding of Goods

It means the Common Schedule for the Classification and Coding of Goods for the Gulf Cooperation Council Countries adopted pursuant to Cabinet Decision No. 119 of 2024 referred to above or any legislation that amends or replaces it.

| |||||||||||

Revised Provisions under Article 2 of Ministerial Decision No. 265 of 2023 | |||||||||||||

Treasury & Financing Services | The scope was limited to providing treasury and financing services only to Related Parties. | This has been broadened to cover treasury and financing services to Related Parties or for its own account. | |||||||||||

Trading of Qualifying Commodities | Earlier Trading of Qualifying commodities included 1. Physical trading of Qualifying Commodities. 2. Associated financial derivatives trading used to hedge risks from such activities. | Now, Trading of Qualifying Commodities means: 1. Physical trading of Qualifying Commodities. 2. Associated financial derivatives trading used to hedge risks from such activities. 3. Associated structured commodity financing activity. Provided this activity cannot be conducted by a Qualifying Free Zone Person if revenue from distribution, warehousing, logistics, or inventory management functions is 51% or more of their revenue for the relevant tax period. (structured commodity financing activity shall include prepayment, factoring, forfaiting, countertrade, warehouse receipt financing, export receivable financing, project finance, Islamic trade finance, and streaming financing) | |||||||||||

Reinsurance Services and Insurance Activities | Earlier, Defined under Federal Law No. 6 of 2007. | However under recent updates, it has been now regulated under Federal Decree-Law No. 48 of 2023. | |||||||||||

Distribution of Goods (Designated Zone) | Earlier, ‘Distribution of goods or materials in or from a Designated Zone’ applied only to customers who resell, process, or alter such goods or materials, or parts thereof, for the purposes of sale or resale. | Distribution of goods/materials in or from Designated Zones (DZs) will be treated as a qualifying activity, including when involving Public Benefit Entities (PBEs).

For qualification, distribution should be either to customers who will resell the goods or to a PBE. | |||||||||||

Publication and Application of this Decision | This decision shall come into retrospective effect on 1 June 2023. | ||||||||||||

List of Recognised Price Reporting Agencies

The list attached to Ministerial Decision No. 230 of 2025 on Determination of Recognised Price Reporting Agencies include the following:

Free Zone businesses specially engaged in commodity trading should reassess their eligibility, as the new decisions take effect from 1st June 2023. To evaluate the impact on your business, we kindly request you to share the list of commodities traded, so we can determine whether they now qualify and enable you to benefit from the Corporate Tax @0%.

Search

Recent Insights

Earlier this year, the Federal Tax Authority (FTA) issued Ministerial Decision No. 84 of 2025, mandating certain categories of taxable persons to prepare and maintain Special Purpose Audited Financial Statements for UAE Corporate Tax purposes.

Following this, the FTA has issued Decision No. 7 of 2025, offering clearer guidance for Tax Groups on preparing and maintaining these financial statements.

The decision outlines specific requirements for Audited Special Purpose Financial Statements (SPFS) for a Tax Group, where Aggregated Financial Statements must be prepared by combining the standalone financial statements of the Parent Company and each Subsidiary within the group

While preparing the aggregated Financial Statements of the Tax group, the taxable person should consider the following:

Members Leaving the Tax Group:

The new guidelines will apply to tax periods commencing on or after 1 January 2025.

FTA Decision 7 of 2025 - Audited SPFS for Tax Groups: Key Takeaways

Search

Recent Insights

The Dubai Cassation Court has issued a landmark ruling in Case No. 685/2024, providing critical clarification on the application of Value Added Tax (VAT) to construction supplies and services performed prior to the implementation of VAT in the UAE on 1 January 2018. This decision has significant implications for contractors, developers, and other stakeholders involved in long-term construction projects that span the VAT implementation date.

The ruling confirms a fundamental principle of taxation: VAT cannot be applied retroactively to supplies delivered before the law came into effect, regardless of when the associated invoice was issued or payment received.

VAT in the UAE was introduced under Federal Decree-Law No. 8 of 2017, which came into force on 1st January 2018, along with the Executive Regulations (Cabinet Decision No. 52 of 2017). This legislative framework set out the mechanisms for identifying taxable supplies, VAT treatments and determining the date of supply.

There was considerable uncertainty in the construction sector regarding multi-phase, multi-year contracts during the transitional period following the introduction of VAT. Key questions arose about how VAT should be applied in the following scenarios:

The case before the Dubai Cassation Court involved a contractor who had entered into a construction agreement prior to 1 January 2018. Although portions of the work were completed and delivered before VAT was introduced, invoices for some of these supplies were issued only after the VAT law came into force.

The Ruling: Key Takeaways

The Dubai Cassation Court reversed the lower court’s decision, stating:

“VAT is not applicable to supplies of goods and services that were completed before 1 January 2018, irrespective of when the invoices were issued or payments received.”

The court cited the following critical provisions:

1. Article 25 –Date of Supply

This article outlines that the “date of supply” is generally the earliest of:

The court affirmed that, in cases where supply was demonstrably completed prior to 1 January 2018, that supply is deemed to fall outside the VAT regime.

2. Article 80 – Transitional Provisions

Article 80 emphasizes that VAT is only chargeable on the portion of supplies delivered after the implementation date, unless otherwise agreed contractually.

The court adopted a “substance over form” interpretation, focusing on the actual performance and delivery of obligations, rather than the formal act of invoicing or payments.

This interpretation ensures that parties to long-term contracts are not unjustly penalized for administrative or procedural delays in invoicing or payment processing.

This decision carries significant implications for businesses in the UAE construction industry, as many continue to face unresolved transitional VAT assessments.

Pre-2018 Supplies are non-vatable

Any component of a project—whether labour, materials, or services—that was completed or delivered prior to 1 January 2018 is not subject to VAT, even if invoice issued or payment recei

Accurate Documentation Is Crucial

To rely on the VAT applicability, contractors must retain clear, dated documentation proving when supplies were completed. This includes:

Businesses that may have erroneously charged or paid VAT on pre-2018 supplies due to ambiguous billing practices or FTA assessments may now have grounds to:

The Dubai Cassation Court’s ruling in Case No. 685/2024 sets an important precedent in the interpretation and application of VAT in the UAE, particularly during transitional periods. It provides a fair and pragmatic solution for the construction industry—a sector heavily impacted by long-term contractual obligations.

Furthermore, it is essential for contractors, developers, and legal advisors to align their contractual, accounting, and compliance practices with this interpretation. Maintaining proper documentation, ensuring clear communication with clients, and engaging in proactive tax planning are key to avoiding disputes and ensuring VAT compliance in the post-2018 UAE tax environment.

Summary of the Dubai Cassation Court VAT Ruling (Case No. 685/2024)

Search

Recent Insights

The UAE Federal Tax Authority (FTA) offers a VAT refund scheme to UAE nationals constructing new residences. This initiative aims to alleviate the financial burden of VAT on construction costs, promoting homeownership among Emiratis.

A ‘residence’ refers to any building—such as a townhouse or villa—mainly used as a private home by an individual. It must include basic living features like a kitchen, bathroom, sleeping areas, along with any fixtures or fittings that come with it.

Additions or separate buildings built later on the same plot are not considered part of the original residence for the New Residences Refund Scheme, unless they independently meet the definition of a residence (i.e., have their own kitchen, bathroom, and sleeping areas).

Examples

Properties registered for commercial use, like hotel apartments, do not qualify as ‘residences’ under this scheme.

Eligibility Criteria

Eligible Expenses

Expenses must relate to a newly constructed building which is to be used solely as a residence of the applicant and / or his or her family. VAT on transport and clearing agent fees can be refunded if they are directly linked to building materials used to construct a private home for a UAE national or their family. The materials must be fixed to the building in a way that they can’t be removed easily without tools or causing damage. No refund is allowed for costs related to extra or separate structures unless they qualify as a full residence on their own.

A list of what expenses are covered and not covered is provided below:

Expense items eligible for refund

Expense items NOT eligible for refund

The refund application must be submitted to the FTA within 12 months from the date the newly built residence is completed which is the earlier of the date:

The applicant must provide proof of the date the residence was occupied. In certain situations, like illness, military service, legal disputes, or pending construction work, the 12-month deadline can be extended. These events must be supported by official documents, and the FTA will decide if the reasons are acceptable. It should be noted that refurbishments or changes to previously completed work are not considered in this context.

To apply for the New Residence VAT Refund, applicant must submit their application through the FTA E-Services Portal. If they don’t have an account, they need to register first then proceed for refund application by following below mentioned steps:

Step 1

Where the FTA checks the application and may ask for original or extra documents. Only one refund request can be made per residence, unless it includes a retention payment, which allows for a second claim.

Step 2

If the application meets the basic conditions, it moves to next step, where it’s sent to a Verification authority within five working days. Applicant will be given a reference number and may need to submit more documents. The Verification authority will carefully review the expenses and VAT claims.

Procedures & steps:

Documents required

If the request is preliminarily approved by the FTA, the authority will e-mail the applicant requesting additional documents.

Additional Documents which may be requested by FTA

The Verification authority may request additional documentations, or original of documents, to complete verification procedures. Reviewing the documents and making payment might take up to 20 business days from the date all required documents have been submitted.

If a UAE national needs to make retention payments to contractors after the new residence is completed, this should be mentioned in the initial VAT refund application. Once the payment is made, a separate VAT refund claim can be submitted within 6 months of the payment date, along with proof of payment (e.g. a receipt).

Note: A claim may not be made in connection with a building that will not be used solely as a residence, for example as a hotel, guest house, hospital or for other similar purposes. Should the building be used for any purpose other than being the residence of a UAE National after receiving the special refund, the FTA will require the applicant to repay any VAT refunded to him as a result of breaching the above condition.

The FTA has launched the “Maskan” application in 2024 to simplify the VAT refund process for UAE nationals building new residences. This digital platform allows users to upload and link invoices, track refund status, and manage claims directly through the app. It reduces paperwork and speeds up the process. The app is available on iOS and Android and requires login via UAE Pass.

Search

Recent Insights